Most of our society is reliant on financial products and services. As a result, it forms the backbone of a country. The financial services industry is frequently associated with resistance to change and strict restrictions.

Some of the technologies used are no longer relevant in the twenty-first century. To adapt to the paradigm shift of the ever-evolving information era, these legacy systems must be overhauled urgently.

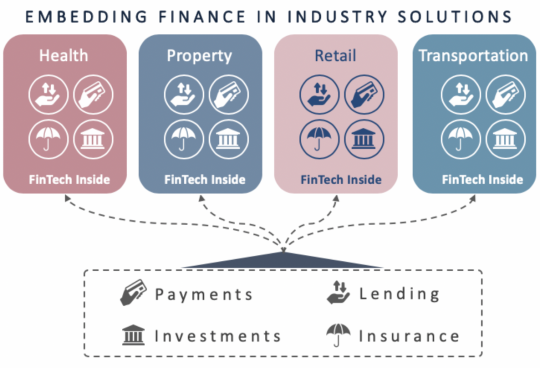

Financial service providers will no longer be seen as a separate and distinct industry, but rather as one that is embedded in every product and service. The financial services industry has been compelled to reconsider its business strategies because of the COVID-19 outbreak. It has persuaded businesses to embrace embedded finance as the Fintech of the future.

Embedded Finance vs Embedded Fintech

Financial services have been embedded into a wide range of software and applications sold by non-bank suppliers in recent years. According to a report from Cornerstone Advisors, banks can create another revenue stream from new products and services already created by Fintech start-ups.

This is called embedded finance and is quickly becoming one of the most disruptive trends in payments, banking, and technology today. Embedded finance is altering the financial services distribution model and giving tech companies a new position in the financial lives of people and businesses.

The difference between embedded finance and embedded Fintech is the direction of the service.

Embedded finance is about enabling non-financial services companies to provide banking services. Embedded Fintech, on the other hand, is the integration of Fintech products and services into financial institutions’ product sets, websites, mobile applications, and business processes.

Bill negotiation services, subscription management, data breach and identity protection, wealth transfer management, and cryptocurrency investing were all recognised as embedded Fintech prospects for banks in a study conducted by Cornerstone Advisors.

Customer experiences are nowadays expected to be seamless and easy to understand. Embedding services save time, are more convenient, and strive to improve the client experience dramatically. Customers want to be more empowered and independent while making decisions in the digital age.

Embedded finance tries to achieve this by putting power in the hands of customers and allowing them to make financial decisions at their leisure rather than being forced to do so by financial institutions.

Image: Rosenblatt Securities

Rise of machine learning and Artificial Intelligence (AI)

When a company provides a wide range of embedded finance services, it may believe it is effective. The amount of embedded finance solutions, however, isn’t the only deciding element. An organisation must determine which embedded financial solution best meets its needs. Embedded financial products will grow if the right balance is found.

How can we figure out what the best blend is? We don’t have to do anything manually anymore, thanks to AI and machine learning, since it will aid in the collection and analysis of industry-specific data points, as well as the selection of acceptable customer solutions.

Access to data

According to CB Insights, traditional banks and lenders are frequently used by firms seeking loans, and creditworthiness is determined through extensive processes. These loans are frequently accompanied by exorbitant fees and interest rates.

Non-financial businesses, on the other hand, may have access to data that banks do not, such as purchase categories, frequency of purchases, and top-selling merchants. This information enables them to provide borrowers with more accessible, personalised, and affordable lending options via their platforms.

Nonbank financial services, such as bank accounts or wallets, payments, and lending services, are becoming more widely available. The companies’ adoption of embedded finance—banking-like services provided by nonbanks—is intended to keep consumers and boost their “lifetime value.”

The competitive advantage of data-rich financial institutions will erode when the data layer is open.

The BaaS imperative

To fulfil the growing need for embedded finance, financial institutions are increasingly offering banking as a service (BaaS), which consists of packaged products, frequently white-labelled or co-branded services that nonbanks can utilise to serve their consumers.

Because BaaS is typically provided to customers via APIs and requires robust risk and compliance monitoring on the part of the embedded financial partner, it will necessitate new technologies and skills to make it work.

Many banks are concerned that delivering their products through partners may jeopardise their customer relationships. However, if end users begin to adopt embedded finance in large numbers, banks may have little alternative but to develop BaaS business lines.

The good news is that allowing partners to market banking products can be a high-volume, low-margin business for banks. Banks commonly struggle with their cost structures, which are often built on old technology and supported by human processes and operations. Banks must undertake digital revolutions to provide BaaS, but many have already done so.

Banks should adopt a BaaS strategy right away, based on a realistic assessment of their cost structure and transformation route. They should also understand the implications on their operations of a major increase in client demand for embedded banking experiences.

Banking as a service and API banking could become as ubiquitous as online or mobile banking, a channel that every bank needs to build and maintain.

Is embedded finance the future?

The future will see a gradual and painless entry into the world of embedded finance. Because of its adaptability and interconnection, embedded finance will continue to exist. It will open new possibilities and bridge the gap between different industries and their relationships.

The involvement of large technology businesses in modernising the financial services landscape will be critical. Companies should be willing to collaborate to expand the market. Businesses must embrace change to thrive and differentiate themselves.

Appello offers custom financial software development services that anyone can use with ease. We create Enterprise-grade technology with the intuitive experience of a consumer application which can amplify the level of user experience to meet any specific business requirements. Contact Appello today.